Year to Date Statistics (through June 30, 2018)

MSCI International Index -2.75%

Long term bonds -4.25%

Preferred Stock index down -1.19%

The Virtue of Worry

Worry is suffering felt for an injury that has not yet and may not happened, but we worry anyway. In finance, worry is a useful tool. A worry wart is well suited for the financial world-he/she is unlikely to plunge or become over confident. Financial Planning and investment positioning involves worrying about what could go wrong. In this report, we will examine some factors supporting this bull market and others that are threatening to the current forward momentum. Many factors can cripple the forward march of an army: dwindling supplies of fuel, inability to find food, second rate technology in weaponry. During World War II, Patton’s lightening progress through Europe and toward a reeling German military late in World War II was halted largely due to supply shortages. On August 28, 1944 Patton summed it up this way: “At the present time our chief difficulty is not the Germans, but gasoline. If they would give me enough gas, I could go all the way to Berlin!”. At the same time, the Germans themselves were suffering from a lack of fuel. In a similar vein, financial expansion draws its fuel from multiple sources. Right now, the economic expansion is being propelled by a surplus of available investment cash, corporate buybacks, and consumer optimism fueled largely by the highest employment rate since the year 2000[1].

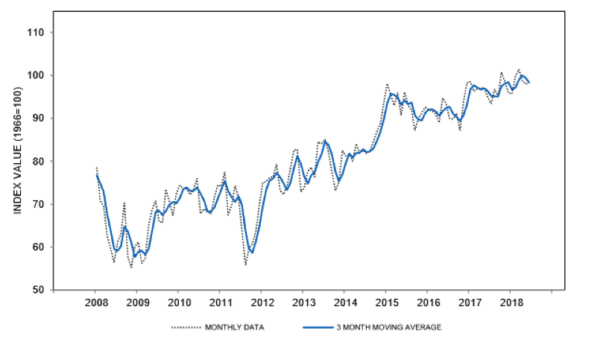

Not surprisingly, consumer optimism, and by extension investor optimism is currently strong:

Source University of Michigan

However, a large contingent of business people does not like the implications of a tariff war, and this has stopped portions of the equity market in its tracks. History has shown protective tariffs lead to tit-for-tat behavior between trading partners. Even if the current administration is successful in pressuring certain countries, notably China to lower barriers to U.S. products, a sense of uncertainty may well be delaying capital expansion projects that would otherwise keep the current economic growth cycle going. How worried should investors be?

So far, the market is taking potentially disastrous news in stride. Sure, volatility is up from recent years, but really, it has only returned to “normal” levels:

Similarly, year-to-date, returns for stocks are pretty much in line with long term trends, although the NASDAQ index, heavy with technology companies has significantly outperformed the broad averages. There are no overt signs of an impending collapse for equity or bond values, only a long list of worries…and what year has lacked worry? We get paid to worry for you, so, anticipating a normal summer swoon have shifted to the largest allocation to short term fixed income assets in ten years. That said I suspect we will be proven too cautious by year end.

Here are the positive economic developments that have, so far overcome fear and uncertainty in the minds of investors:

The Dollar rose some 5% in the past quarter, a stunning performance. This appears to be the result of a combination of factors. First, the USA is the only major financial zone with attractive short term interest rates on liquid fixed income investments, making it a good currency in which to park cash[2]. Then there is the probable effect of repatriation. With corporate income tax rates slashed to their lowest level in modern history, companies with well-known stashes of un-taxed profits held abroad are now bringing home the bacon – the Wall Street Journal estimates this at about $175 BB in the first half of 2018. There is plenty more where that came from, and estimates I’ve seen are that another $200BB or so may find its way back to the US this year, which helps strengthen the dollar. A rising dollar can create a virtuous cycle where foreign investment funds favor U.S. equities because the strengthening dollar offers some cushion even if the U.S. stock market is not roaring upward.

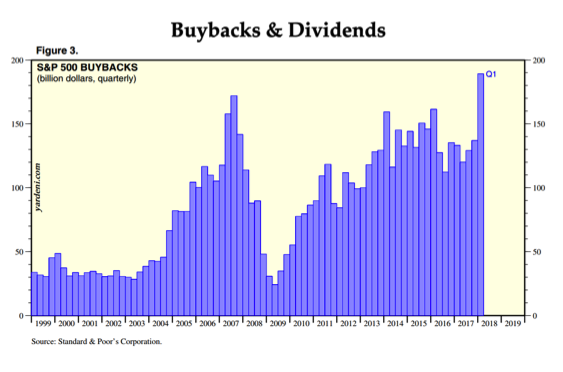

Stock buy backs – With operating profits strong and funds returning to our shores from repatriation, stock buybacks were happening at a record pace last quarter, and are expected to repeat or exceed the performance when statistics for this quarter are published. Buy backs tend to create capital gains for shareholders by reducing a company’s float of common stock. Buy back activity appears to have supported the technology sector more than old line firms, because tech firms, notably Microsoft and Apple were diverting profits to overseas subsidiaries for years. A significant amount of that money is flowing home and into share repurchases.

Four years ago, we recommended Apple as a buy. Our reasoning was that this “maturing” company’s sales would slow yet it would succumb to investor pressure to raise its dividend. In fact, Apple has raised its dividend, up 55% in the past four years. Apple reported at its May quarterly analyst conference call that it will be spending an additional $100BB buying back its stock, which is supportive of not only the share price of AAPL but of the market in general. We continue to own the stock for many clients.

U.S. Manufacturing sector is strong. The Wall Street Journal reported on July 3 that manufacturing was accelerating in the last two months of the quarter, and although this is a coincident indicator, the acceleration trend appears predictive of expanding economic activity, certainly not a slow-down. It is anticipated that June Employment will increase by 175,000 jobs, a strong figure.

When will the party end? Perpetual bears have been trying to talk the market down for nearly a decade. The amount of money left on the table by people who believed their tale of woe is criminal. The aftermath of the Great Recession was, in retrospect an opportunity to go “all in” with stocks, but being rational and careful, we instead found quality corporate and municipal bonds with yields well above inflation. Many clients still hold issues purchased in that period, with nominal yields that exceed anything available from more recent issues[3]. In those post- “Crash” years, 2009, 2010, 2011 a value investing approach suggested that besides bonds, nibbling on some tasty stock opportunities were a worthwhile risk. We’ve booked profits on many of these holdings in the past decade. Still, the forces that will possibly slow the party are already in place: rising short term interest rates, labor shortages, rising volumes of risky debt and trade spats. Ominously, an imbalance in supply vs demand is pushing up home prices in some of the same markets that collapsed ten years ago: Miami, Phoenix, Las Vegas. But we believe that before the next recession, the odds are we will have another leg up for stocks, especially if the current trade disputes are resolved (and they may well be resolved, despite current posturing by the parties).

Why? The financial sector is poised for a run of growing profits, despite headwinds from interest rates. Banks are being given freer rein to make loans, pay higher dividends and buy back stock. The financial sector is a major portion of stock indexes, about 15% or nearly $8 TT (source: www.thebalance.com). Technology, now representing 25% of the broader index, does not appear to be endangered. Although tech is not cheap, it is nowhere as overvalued as in the lead up to the Tech Wreck, and as mentioned earlier, this sector is still being helped by share buybacks. Between them, these two promising sectors represent 40% of the capitalization of the Standard & Poor’s 500.

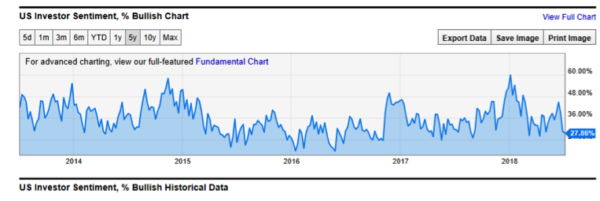

Importantly, investors are not yet over-confident nor are they ebullient. Note that investor sentiment lies about in the middle of the range of bullishness of the past five years:

Source Y Charts

Looking Ahead

The S&P 500 has closed at its calendar year high in the second half of the year (i.e., during the 6 months of July-December) 74% of the time since 1950. In 15 of the last 25 years, the index’s calendar year high has occurred during the month of December. Over the last 25 years (i.e., 1993- 2017), the S&P 500 has produced an average gain of +9.7% per year. The first 6 months of the year (i.e., January-June) have gained an average of +4.5% over the last 25 years. With a steady flow of uncertain and threatening news, the broad stock index has underperformed year to date, but amazingly has not sunk to negative levels. So far this appears to be a relatively normal year in terms of equity index performance, and history suggests we may end the year on a high note. [4]

Are Rising Interest Rates the Death Knell for a Bull Market?

It’s pretty well established that valuation of equities is, in part, a function of the cost of money. When competing instruments, primarily bonds are offering attractive yields as compared to stocks, money tends to get squirreled away in fixed income instruments, sapping fuel from the stock market. Perhaps it is surprising, therefore that despite a significant increase in yield for ten year Treasury bonds, the market has been generally strong since late 2016 (in the graph below, T-Bonds are the black line while stocks, as represented by the S&P 500 index are represented as the red-and-black weekly range.) Until stock market yields are swamped by T-bond yields perhaps if they rise toward 4%, interest rates are unlikely to be a threat to this bull market.

So, in a quarter that has seen the eruption of a trade war and rising interest rates, a market that faces the uncertainties of an election later this year, the fact that markets have corrected little seems to be evidence of an underlying strength that bodes well for investors. Below is the S&P 500 adjusted for the distortions of inflation. When it rose to a historic high near the end of 2014, we became more convinced that we are in the throes of a “secular” period of rising equity values. Subsequent market behavior appears to confirm that the new high reached in 2014, after a 16 year period of price consolidation and, of course, the worst correction in two generations, is a sustainable trend.

We proceed with a cautious position, but remain overall optimistic about the remainder of 2018.

Gary E. Miller, CFP

[1] The last time unemployment was lower was 1969!

[2] We have recommended moving a significant portion of client cash into overnight traded short term money funds whose yield is now above 1.7%

[3] Some of these holdings, as they near maturity are candidates for sale, as “yield to maturity” may no longer be attractive

[4] BTN Research, a service of MFS funds group.