Given the worrisome headlines and market volatility clients are seeing some stepped up trading activity for their accounts. It feels like a good time for a brief update.

I sold out our position in the big bank exchange traded fund. This was bought a few weeks ago based on a loosening regulatory environment and strong bank balance sheets, which offered the prospect for stepped up share repurchases and/or dividend increases. But, emergence of problems in the private equity space, have led to big banks to become suspect, because they may have loaned money to some of these aggressive and obscure investment pools. This was a characteristic of the losses for banks during the Great Financial Crisis. War in the Middle East has not improved sentiment, so with the price trend turning downward I decided it was better to be safe than sorry. Every client took a loss, but a small one.

Here is a recent graphic outlining exposure of important major banks to private equity:

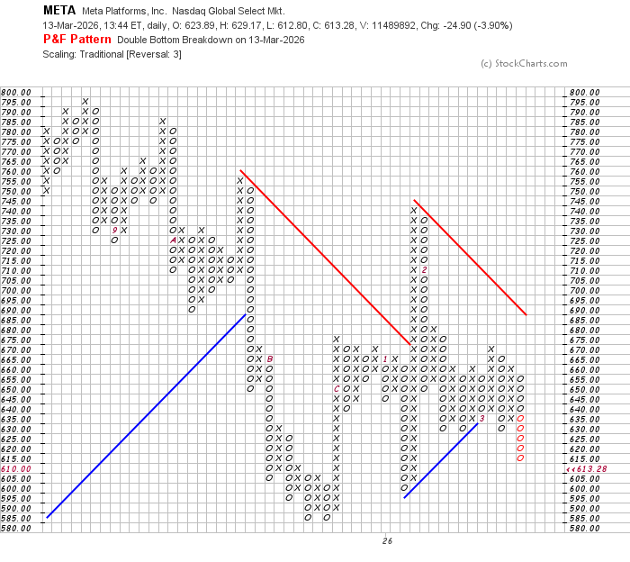

I also liquidated our clients’ position in Meta (Facebook) this week. Below, this “Point and Figure” chart of Meta shows the breakdown on March 13 that to me is a harbinger of further deterioration to come. The company is spending enormous amounts building data centers and A.I. infrastructure. They are borrowing money to do so. This may prove a successful long term strategy, but also removes the possibility of share repurchases. Chart action was enough to convince me this is now a high risk holding. Nearly all clients booked a profit.

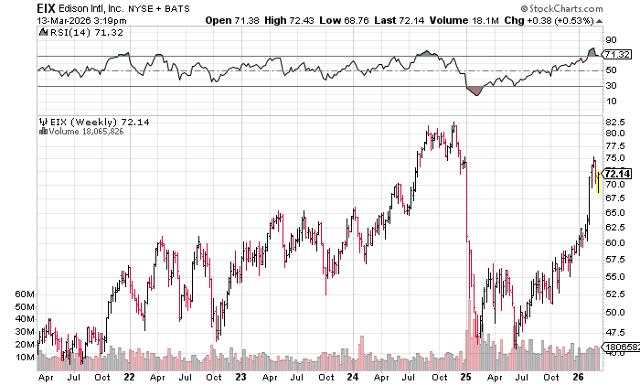

On the positive side, we were buyers of a high yielding bond from an issuer whose name may be a bit suspect in Southern California: Edison International (EIX), parent of Southern California Edison. The lawyers tried to assign blame for the terrible Palisades fire that destroyed an expensive neighborhood in Los Angeles county in early 2025, but investigations do not support this accusation, rather arson was the generally agreed cause. Still, EIX and associated securities took a big hit as investors bailed before it was clear who might be responsible. Further, the company does have exposure to the Eaton fire, which is going to cost the at least $1BB. This situation apparently allows Edison to access California’s Wildfire Fund, designed to protect public utilities from disastrous economic exposure. The final cost to shareholders will not be determined for years, but it is instructive to note that institutional buyers have returned to the common stock, which has recovered most of the losses from early 2025:

While I’m not confident enough in this situation to buy the common stock, there is an attractive preferred stock with a nominal yield of 7.5%. Recall that preferred stock has a superior position to common stock in the financing hierarchy of a corporate issuer like Edison. We have added that to client porfolios, as it satisfies my desire to lock in higher yields at a time when money fund yields have been falling to the low 3% range.

The series M preferred was issued in late 2024, shortly before the fires and as you can see, had grown to a nice premium price until the fire caused a panic. This preferred has recovered along with the common, and over time may go higher still. I feel that picking up the preferred at just above its par value of $25.00 with an effective yield of 7.47% will prove to be a wise source of income. (see chart below)

I hope this update finds you well and happy, and I will provide a more detailed quarterly report in about three weeks.

Gary Miller