Fear Street

A year and a quarter that started out strong ran out of gas as the Federal Reserve failed to lower interest rates and as a military action (“excursion” “war”, call it what you will) resulted in strangulation of one of the most important channels for waterborne transport of oil, liquified natural gas, fertilizer and helium. Although the United States is self-sufficient in most of these commodities, Europe, Asia, South America, and Africa are not. With a global economy and supply chain that are integrated, the situation is affecting a wide range of industries and not in a good way.

The broad S&P 500 Index shed 7.3%. Other than energy producing companies in the United States and some consumer staples, no sector was spared: Tech stocks were off 11.4%, health care down 7%, even normally stable Utilities fell 7.6%. Foreign stocks suffered, but generally not as much as in the USA where indexes are weighted toward big technology firms. Our client portfolios are individually developed, but in general we saw these balanced portfolios produce gains or losses of around 2%.[1] Most clients have a significant allocation to fixed income (bonds and preferred stock) and these held up well and continued paying interest. I found a couple of opportunities in this sector for many client portfolios.

One of our most successful investments of 2025, Gold, was hammered in March, giving up 14.3% but still up by about 4.6% so far this year. Gold is often a hedge against a depreciating US dollar, which enjoyed a so called “flight to safety” that came with war: the US dollar rose 3.5%. Given that the US has a debt level approach $ 40TT, it is remarkable that the dollar is still considered a safe asset by some.

Silicon Sell-off

Pretty much everyone knows the silicon semi-conductor (chip) story: insatiable demand for high speed processing has led to a secular bull market going back to the tail end of the Covid Era. Below is a chart of the VanEck semi-conductor exchange traded fund (SMH), widely held by clients. An investor position in this vehicle has more than tripled the investment in five years. It is important to note, however, an agonizing correction was felt along the way, which lasted for ten months. The recent sell-off could well match that of ’24-’25. There is a capacity shortage in the industry and so they are investing heavily to expand, which will likely pinch free cash flow for a while. Also, I am nervously watching the helium situation. Who knew that Asian chip producers like TSMC (Taiwan), SK Hynix and Samsung (Korea) rely on helium gas which is liquified in Qatar and shipped through the Straits of Hormuz, to produce wafers.

Qatar is responsible for 30-38% of the world’s helium production. A company like Taiwan Semiconductor Manufacturing, which fabricates GPU-style semiconductors for Nvidia, for example, requires Helium to make this product. A shortage of helium will likely reduce production levels, hurt sales for both TSMC and Nvidia (among others) and further, this will slow completion of the scheduled, furious build out of A.I. data centers. No wonder semi-conductors and related industries are sliding![2]

The Banks

Back in July and August of last year, I sensed that bank regulation would be reduced under the Trump administration and began positioning in an exchange traded fund of big banks as well as, for some, shares of JP Morgan (JPM). This is based on the belief that the current administration in D.C. is receptive to pleas for reduced regulatory burdens, which were imposed following the near collapse of our financial system in 2007-2009. Last summer’s supposition has proved correct, and on paper we made a nice profit. However, beginning in February, another, ominous thought was applied to the banks. A respected banker, Jamie Dimon of JP Morgan expressed concern about private equity and shadow banking. Dimon’s worries were brought into stark focus when a leading private partnership, Blue Owl, limited withdrawals by partners, a sign that a) There is a wave of investors exiting the partnership and/or b) the investments they own cannot be readily liquidated to satisfy cash distribution requests. Banking and financial companies run on trust. Some big banks have extended loans to private equity partnerships who lend to small, often start up, enterprises. These investments lack the liquidity of publicly traded companies, meaning, that as the Eagle’s song “Hotel California” suggests “you can check in any time you like, but you can never leave.” Private equity promises sky high returns at the price of lost liquidity. Cue the promoters who recently have begun to offer entry to the “exclusive” private equity space to retail investors. When retail begins piling into a sector, a top is usually near. Suddenly investors in private equity limited partnership are asking for their money back and being told they must wait.[3] When one or two of these entities refuses to give clients their money back, word on the street spreads and there is a run for the exits.

This has led to worries that the private equity stress could spread to big banks.[4] Our investment in KBWB began a precipitous decline in early March. With that, we exited, taking small losses. I just hate it when a profitable position turns into a loss, but fortunately the losses were small and I for one am sleeping better at night. As if to confirm my fears, on the last day of this quarter, the legendary Warren Buffet, interviewed on CNBC, when asked about bank risk, gave this haunting reply:” “It’s all parts of the banking system because they all affect each other, and the troubles from one can spread over to another. What I really would care about is the stability of the banks.”

Redeployment out of Tech

For some clients we sold out of such tech names as Meta (Facebook) and reduced exposure to Microsoft, Nvidia, Amazon, and Arista Networks. This was done, not because we think tech stocks are fundamentally a bad bet, but because investor sentiment, as reflected in technical performance suggested the risk to reward metrics have deteriorated.

The fundamental story behind this weakness goes like this: companies like Meta, Amazon and Microsoft are investing enormous dollar amounts into the purchase of land and construction of data centers for the A.I. world of the future. Because no-one wants to be left behind, this land rush is causing companies to overspend, with return on investment uncertain and perhaps many years away. Bears cite the Tech Bubble of the late 1990’s. We were promised miracles from the new “World Wide Web.” In fact, many of the predictions came true, with Amazon (AMZN) a shining example. After six years of plowback, that is, reinvesting cash flow into growing the business, Amazon was finally able to report profits.[5]

Today Bears suggest that, as in the .Com era, investment into data centers and A.I. inference models, may not bear fruit for many years. As this realization rolled through the markets and tech shares sagged, I felt that, in some cases, it was time to take money off the table. Most client holdings of tech that were sold booked a profit upon sale.

Your portfolio still contains a lot of technology related stock exposure, and I believe the long term future for these companies is bright. But part of my job is managing volatility, and these companies tend to exhibit high volatility.

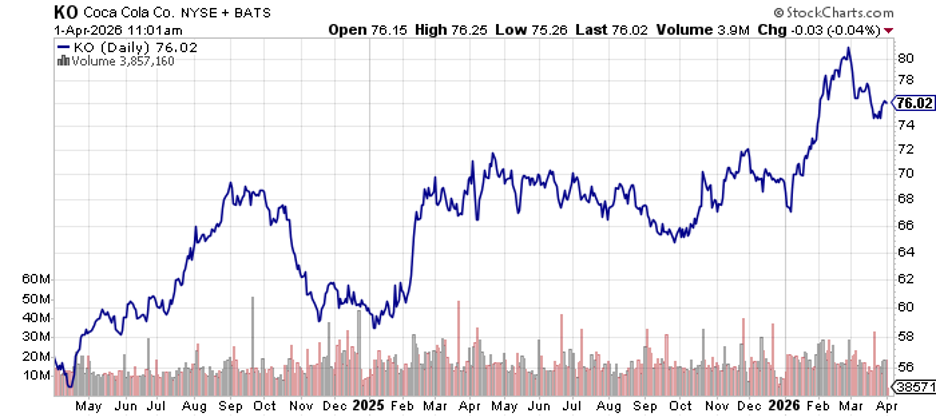

Contrast tech to one of the most reliable free cash flow producing companies that I found at a bargain price, Coca Cola (KO). While there is no one catalyst that makes this company likely to soar, I felt it should benefit from two things in 2026: the flood of tax refunds[6] that is expected to drive consumer spending and continued weakness of the dollar The company has raised dividends every year since the mid 1970’s. The company derives a little over half of its revenue and profits from international (non-dollar) sales. Given my belief that the US dollar may weaken further, this can help earnings reported in dollars. Soda consumption is growing slowly, Coca Cola’s top line growth is slow, perhaps 1% to 2% per year but it has been raising its net operating income by some 5-6% in 2025 by price increases and efficiencies by becoming more of an “asset light” enterprise. Since our purchase, the sharp rise for gasoline prices means consumers now have to spend more of their tax refunds on gasoline, which causes me to worry about my hypothesis that tax refunds will accelerate consumer spending. So far, however the correction from recent highs is modest.

Verizon, a dividend leader, surprised this quarter. I picked it up for many client portfolios based on its dividend level of about 6% during 2025. To my delight the stock popped in February as new leadership at the firm drove investor confidence that the company can stop losing prepaid customers to the competition and improve profit margins.

Promising News

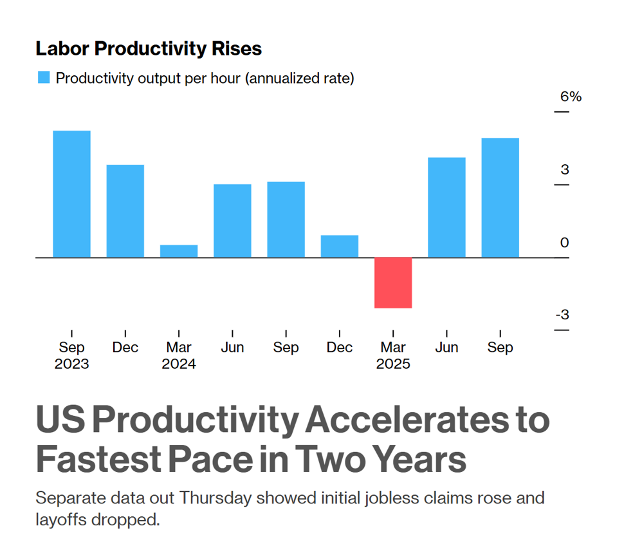

Productivity is improving. While most economists feel it is too soon to thank artificial intelligence, I suspect, based on my own experience, that it is making workers, especially knowledge workers faster and more efficient. Why is productivity important? It offsets inflationary spending- when a worker is able to produce 8 widgets per shift as compared to 6 widgets, the cost per widget declines and is, hopefully, passed on to the ultimate consumer. The Federal Reserve, following its mandate to control inflation, watches productivity trends closely.

Conclusion

The uncertainty in markets has seen some liquidation of your more volatile positions, redeployment into some high yielding bonds and preferred stock with a generous amount parked in overnight money market funds that offer an inflation beating yield of 3.5% or so. However, we end the quarter on the cusp of a bear market. You may see your portfolio value shrink if things continue to deteriorate, but I feel you are in a healthy position, well diversified and holding quality investments that will recover nicely when the recovery comes, as it will.

Gary Miller

[1] More aggressively invested portfolios were generally down by low single digits while more conservative holdings rose slightly.

[2] Consequences from Helium embargo Hormuz:

[3] Blue Owl and Blackstone have both “gated” liquidations, meaning they are telling their investors they can only receive a portion of requested funds.

[4] https://www.nytimes.com/2026/03/14/business/private-credit-jamie-dimon-cockroaches.html

[5] The company went public in 1997 but did not report a profit until 2003.

[6] Analysts believe that as a result of over-withholding from paychecks and due to changes in the 2025 tax rates as the result of passage of the OBBA over $100BB in refunds will be coming to W-2 wage earners in 2026.